Financial Services

Financial services refer to services provided by the finance industry. The finance industry encompasses a broad range of organizations that deal with the management of money. Among these organizations are banks, financial planners, insurance companies, intermediaries, asset management companies, stock brokers, investment funds and some government sponsored enterprises.

Mutual Funds

A mutual fund is a pool of money, which is collected from many investors and is invested by an asset management company to achieve some common objectives of the investors. In practice, funds are generally distinguished from each other based on their investment objectives and the type of securities that they invest in. The broad classification is Debt Funds, Balanced Funds & Equity Funds.

Mutual funds seek to mobilize money from all possible investors. Various investors have different investment preferences and needs. In order to accommodate these preferences, mutual funds mobilize different pools of money. Each such pool of money is called a mutual fund scheme. Every scheme has a pre-announced investment objective. Investors invest in a mutual fund scheme whose investment objective reflects their own needs and preferences. The primary objective of various schemes stems from the basic needs of an investor, viz., safety, liquidity, and returns.

Mutual funds can be classified in multiple ways. Funds can be classified based on the investment objective, as discussed earlier. We have different types of mutual fund schemes growth funds, income funds, and liquid funds. The names of the categories suggest the investment objectives of the schemes.

With a view to bring in standardization in the classification of mutual funds and to ensure the schemes are clearly distinct from one another, SEBI issued a circular on Categorization and Rationalization of Mutual Fund Schemes in 2017. The objective was to bring uniformity in the characteristics of similar type of schemes launched by different mutual fund houses so that the investor can objectively evaluate the schemes chosen for investment. Accordingly, there are five broad categories of mutual fund schemes. Within each category, there are many sub-categories:

A. Equity Schemes (11 sub-categories)

B. Debt Schemes (16 sub-categories)

C. Hybrid Schemes (6 sub-categories)

D. Solution Oriented Schemes (2 sub-categories)

E. Other Schemes (2 sub-categories)

Insurance

Insurance is a financial risk management tool in which the insured transfers a risk of potential financial loss to the insurance company that promises to pay a sum assured for occurrence of an unfortunate event and insured promises to pay a mutually agreed premium.

Contact an expert Know more

Fixed Income Products

Fixed Income Products refer to those types of investment securities that pay investors fixed interest / coupon payments until their maturity date. At maturity, investors are generally repaid the principal amount they had invested.

Contact an expert Know moreLoans

A loan is the lending of money by one or more individuals, organizations, or other entities to other individuals, organizations, etc. The recipient incurs a debt and is usually liable to pay interest on that debt until it is repaid, as well as to repay the principal amount borrowed. There are various types of loans available in the market but they can be categorized into two broad categories, i.e., secured and unsecured loans.

Contact an expert Know more

Equity Research Services

An Equity Research Analyst refers to the person who analyzes financial information along with the different trends of the different organizations or the different industries and then gives an opinion, in his equity research report based on analysis conduct, thereby helping the clients make good investment decisions. Equity research analysts can be classified in two broad categories:

Buy Side: In buy-side, companies have research analysts to help them with investment purposes. They monitor the securities daily and access the impact of macroeconomic news on the long-term performance of the stocks. Additionally, they are in touch with the sell-side research analysts for stock advice and updates.

Sell-Side: Here, the analysis is done to advise the client on the current investment opportunities on the sell-side. The sell-side research analysts analyze equities to recommend buying or selling a particular financial security. These tips are provided to the agent or relationship manager of a brokerage firm and bank in the form of reports prepared by the research analyst.

Retirement Products

Retirement planning is a process of setting retirement income goals and taking all the possible actions and making decisions, which are essential to achieve those goals. Retirement planning includes evaluating sources of income, estimating expenses, and setting up an investment plan or savings plan to achieve the retirement goals by managing the risks and assets.

Annuities: Annuities are popularly known as pension plans. An annuity is the systematic liquidation of an estate – monthly, quarterly, semi-annually or annually, designed in such a way that the investor receives payments periodically. The period during which premiums are paid for the purchase of an annuity is called the accumulation period and correspondingly, the period during which annuity payments are made is called the distribution period. The principal consists of the premiums paid by the person purchasing the annuity, and the interest or appreciation is the amount earned on these funds between the time they are paid and the time they are distributed.

There are two basic types of annuities:

Immediate Annuity: It is an annuity that is always bought with a single premium. Here, one begins to receive payments from the annuity provider immediately. Payment will start immediately at the end of the month.

Deferred Annuity: It is an annuity that can be bought either through a lump sum single payment or through an installment plan. Here, one’s money is invested for a specified period of time until one is ready to begin taking withdrawals, typically upon retirement.

On the basis of payments terms, an annuity can be classified as follows:

Life Annuity: It is an annuity paid through the life of the annuitant, till he/she dies, after which it stops.

Annuity Certain: It provides a specified amount of periodical income for a specified number of years, without consideration of any life contingency.

Joint Life Annuity: It is issued on two individuals, under which payments continue in whole or in part until both individuals die. It is also called joint life last survivor annuity.

Annuity with return of purchase price: It pays back the purchase price of the annuity after a certain period or on death as per terms.

National Pension System (NPS): National Pension System (NPS) is a voluntary, defined contribution retirement savings scheme designed to enable the subscribers to make optimum decisions regarding their future through systematic savings during their working life. NPS seeks to inculcate the habit of saving for retirement amongst the citizens. It is an attempt towards finding a sustainable solution to the problem of providing adequate retirement income to every citizen of India.

Under NPS, individual savings are pooled in to a pension fund which are invested by PFRDA regulated professional fund managers as per the approved investment guidelines into the diversified portfolios comprising of Government Bonds, Bills, Corporate Debentures and Shares. These contributions would grow and accumulate over the years, depending on the returns earned on the investment made.

At the time of normal exit from NPS, the subscribers may use the accumulated pension wealth under the scheme to purchase a life annuity from a PFRDA empaneled Life Insurance Company apart from withdrawing a part of the accumulated pension wealth as lump-sum, if they choose so.

Physical Assets Investments

Physical assets are tangible assets that can be seen, touched and felt, with a very identifiable physical existence. A physical asset is an item of economic, commercial, or exchange value. Physical assets usually refer to gold, silver, real estate and other commodities.

Contact an expert Know moreAlternative Investments

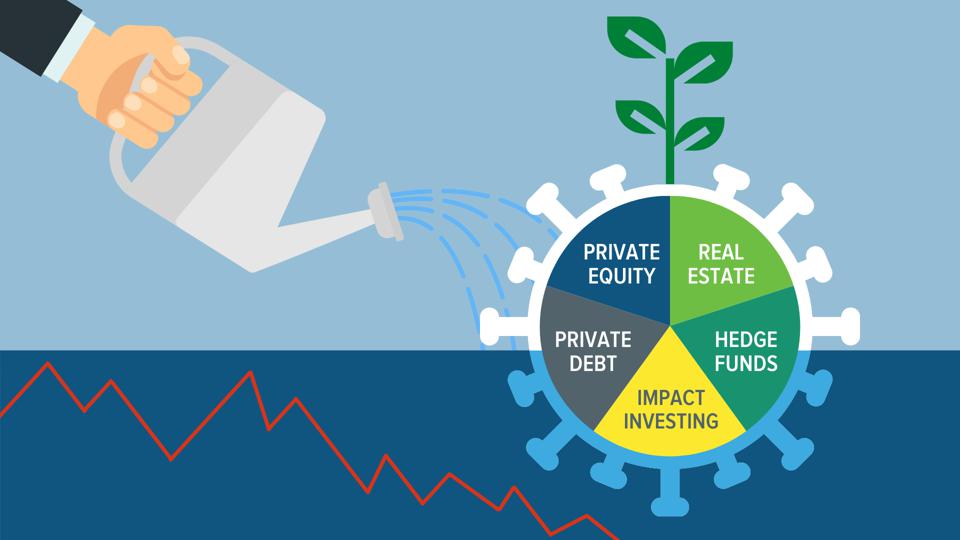

Alternative investments, as the name suggests, refer to investments other than traditional investment classes (i.e., stocks, bonds and cash). It is a different investment class which includes tangible assets as well as financial assets. Examples of tangible alternative asset class are precious metals, art works, antiques, coins, stamps and examples of alternative financial asset class are fractional commercial real estates, private equity, hedge funds and cryptocurrencies.

Alternative investments are mostly held by high-net-worth individuals and institutional investors because of the natural barriers to entry such as its complex nature and lack of transparency (as disclosure requirements are not stringent). Alternative investments generally lack liquidity, which means that it may take time for one to sell off his investments at a fair price and in case he wants sell them urgently, he may have to do it at a substantial loss.

Tax Saving Instruments

Tax planning is one of the ways which can help one to save taxes and increase one’s income. The Income Tax Act provides deductions for various investments, savings and expenditure incurred by the taxpayer in a particular financial year. Following are some of the popular tax saving instruments:

• Equity Linked Savings Scheme (ELSS): Equity-linked savings scheme or tax saving mutual fund is one of the most popular market investment tools among investors with the primary aim of tax saving and wealth creation. This scheme comes with a mandatory lock-in period of three years (the shortest lock-in period amongst every available tax saving instrument in India) on an investment amount under section 80C up to a maximum limit of Rs. 1.5 Lakh.

• Public Provident Funds (PPF): Public provident fund is one of the tax-saving instruments sponsored by the Government of India. However, it comes with a mandatory lock-in period of 15 years (this might harm the liquidity requirements of an investor) on an investment amount under section 80C up to a maximum limit of Rs. 1.5 Lakh.

• National Pension Scheme (NPS): It is one of the tax-saving investments available under Section 80C. Any individual who is a subscriber of NPS can claim tax benefit under Sec 80 CCD (1) with in the overall ceiling of Rs. 1.5 Lakhs under Sec 80 CCE. An additional deduction for investment up to Rs. 50,000 in NPS (Tier I account) is available exclusively to NPS subscribers under subsection 80CCD (1B).

• Life Insurance: Under section 80C, a premium paid on a life insurance policy can be claimed as tax benefit under section 80C within the overall limit of 1.5 Lakh.

Portfolio Management Services (PMS)

Portfolio management is the art of managing different asset classes with the purpose of meeting the investor’s financial objective as per his risk appetite. Appropriate risk-reward relationship, time horizon for reaching the desired financial goals and the amount of capital to be managed are the three basic ingredients of portfolio management.

PMS is a customized service offered to High Net-worth Individuals (HNI) clients. The service is tailored as per the investor’s return requirements and the ability and willingness to assume the risk. An Investment Policy Statement (IPS) is drafted by a PMS to understand the financial position and needs of the client. The portfolio manager ensures that the return requirements coincide with the risk profile. Before executing the optimum portfolio, PMS also studies the various constraints such as time horizon, tax applicability, liquidity, and other unique considerations of the client.

Types of Portfolio Management Services

• Active Portfolio Management: This form of portfolio management aims at beating the performance of a market index such as Nifty. An active portfolio manager will take different positions than that of the tracking index, actively buy and sell securities as per institutional research to create more returns than the index. However, to generate an excess return, the strategy undertakes a higher level of risk.

• Passive Portfolio Management: Such a PMS strategy aims to mimic the performance of an index by investing in the same securities with similar weights. This is known as indexing or index investing. The transaction costs, resulting from securities turnover, are low as compared to active management as the portfolio churning is at a minimum. However, incurring transaction costs leads to an overall return being lower than the tracking index. The returns of the portfolio are pegged to the market returns. Therefore, the variance in returns is low.

• Discretionary Portfolio Management: The portfolio manager is given complete control of the portfolio and is free to adopt any strategy which is suitable to the IPS. Such PMS demands higher involvement for decision making justifying higher fees associated with discretionary portfolio management. This is the best option for clients with limited time and knowledge of investing.

• Non-discretionary Portfolio Management: The PMS will only suggest investment ideas while the investor will be responsible for choosing the recommendation and timing. This employs PMS in an advisory capacity as the final call rests with the investor instead of the portfolio manager.

Estate Planning

Estate planning refers to the organized approach to managing the accumulated assets of a person in the interest of the intended beneficiaries. Wealth may be accumulated with a specific purpose of being passed on to heirs, to charity, or to any other intended purpose. Without formal structures that ensure that these purposes are met, there could be disputes, conflicting claims, legal battles, avoidable taxes and unstructured pay-offs that may not be in the best interest of the beneficiaries. Estate planning covers the structural, financial, legal and tax aspects of managing wealth in the interest of the intended beneficiaries.

The term 'estate' includes all assets and liabilities belonging to a person at the time of his death. This may include assets as well as claims, a deceased is entitled to receive or pay. The term estate is used for assets whose legal owner has deceased, but they have not been passed on to the beneficiaries and other claimants. Once transferred, the estate becomes the assets of the beneficiary who has received the legal ownership. Estate can also be passed on to a trust and managed by trustees, in which case, ownership is with a distinct entity, but periodical benefits from the estate is passed on to beneficiaries. There is no uniform code for civil law that exists in India with respect to this.The consequences of dying intestate are very severe in nature. If a person dies without making a will, he is said to have died “intestate” and in such case his property will be inherited by his heirs in accordance with laws of succession applicable to him.

The end result may not be what the person would have intended. If the dependents include minor or incapacitated children, more than one spouse, elderly parents or in-laws, or siblings and siblings-in-law, there may be disputes in distribution of assets. Distribution of estate may also suffer due to lengthy legal procedures and administration costs. This could add both inconvenience and financial burden to the family. Succession is governed by personal laws, which will apply in the case of intestate death.

Different personal laws apply as follows:

• The Hindu Succession Act, 1956 (Applicable to Hindus, Buddhists, Jains and Sikhs)

• Indian Succession Act, 1925 (Applicable to Christians, Jews and Parsis)

• Mohammedan Personal laws (Governing inheritance of Muslims)

The prolonged dispute, legal battles and costs can be avoided, if intestate death is prevented through timely estate planning.